89% of shoppers are looking to save in the short-term, but only 46% are buying less stuff. The right nudge can lead them to choose you.

If we learned one thing in 2025, it’s the power of resilience. US tariffs, inflation, a government shutdown, and economic headwinds put consumers in a value-driven mindset. But they found ways to keep shopping.

January is a reset for shoppers’ budgets. With economic uncertainty still top of mind, consumers are cautious, but the latest data shows signs of recovery.

To understand how consumer shopping is shifting as we head into the new year, we surveyed 600 US consumers on economic sentiment, spending changes, and how AI is shaping the purchase journey.

The opportunities ahead:

- Many cost-saving behaviors have improved since we last asked in August—and value-seeking shoppers can be won over by building confidence through your messaging.

- “Resolution season” intent is shifting budgets toward personal growth, experiences, and self-care and wellness over the next three months.

- Shoppers are using AI more to help them research, compare, and decide what to buy—and most shoppers are comfortable with brands using AI for personalization.

Read on to learn what these shifts mean for your marketing communications strategy.

5 key actions you can take right now

Before we unpack all of the findings, here’s what we recommend brands do in Q1 based on the data:

- Use value tie-breakers in your messages. Reviews, comparisons, loyalty perks, warranties, shipping speed, and easy returns help shoppers choose you over similar options.

- Offer value-forward alternatives to straight discounts. Promote bundles, bulk buys, subscribe-and-save, free shipping thresholds, and gifts to protect your margins.

- Align Q1 campaigns to “resolution season” intent. Position products through motivations like personal growth, experiences, and self-care and wellness.

- Structure your website for LLMs. Strengthen your website with clear product specs, FAQs, and comparisons so LLMs can showcase your products when shoppers are looking for a product like yours.

- Use AI to scale 1:1 personalization. Amplify relevance in your email, SMS, and push notifications by using AI to improve targeting, timing, and relevance beyond what humans can do alone.

84% are concerned about the economy—but spending is stable

To set the stage: Consumers are still feeling cautious. 84% of shoppers are concerned about the state of the US economy—essentially unchanged from the 85% we reported in August and October.

But that concern isn’t translating into broad pullback.

In the past month:

- 42% decreased spend on discretionary purchases (down from 48% in August)

- 28% increased discretionary spend (up from 20% in August)

While we can’t point to a turnaround in spending habits just yet—as December spending is naturally higher than other times of year—we remain optimistic.

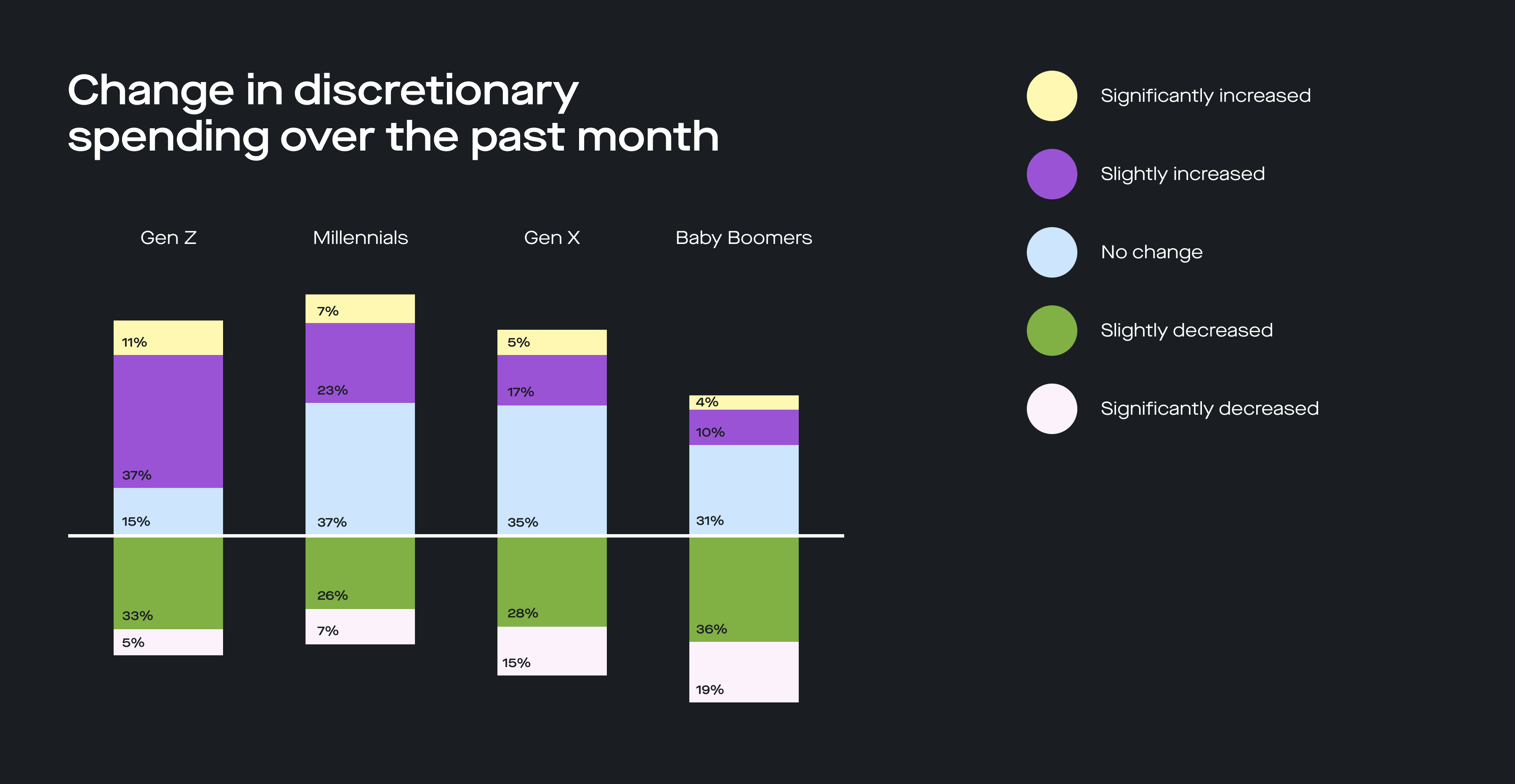

Gen Z is leading the lift: 47% spent more in the past month

Younger generations are more free in their spending, despite being slightly more concerned about the economy than older generations.

63% of Gen Z and 67% of Millennials have spent the same or more on discretionary purchases in the past month, compared to 57% of Gen X and 45% of Baby Boomers.

Gen Z are the ones amping up their shopping the most, though. 47% spent more in the past month, compared to 29% of Millennials.

Gen X’s financial anxiety has cooled since October. This month, 81% of Gen X feel concerned about the US economy—down from 91% during the government shutdown in October, when they were the generation most worried about the economy. This shows how much current events impact their perception.

89% plan to manage costs—but only 46% are buying less

Looking ahead, shoppers are trying to be smart with money—but that doesn’t mean shopping less.

Over the next three months, 89% plan to take at least one cost-management action, yet only 46% plan to buy fewer items (down from 52% in August).

At the same time, 34% of shoppers are taking spend-expansion actions like staying loyal to brands even if there are cheaper options, choosing higher-quality items, and splurging more.

And yes, some shoppers are doing both. These shoppers are balancing saving where they can and spending where it counts.

Perhaps they’re sticking with certain brands they love while choosing cheaper alternatives in other categories. Or buying fewer items so they can treat themselves to something special. Or going premium, but still hunting for the best price in that tier.

One more nuance: Even among those who aren’t concerned about the economy, 62% are still taking cost-management actions. This points to a potential baseline behavior: American shoppers tend to seek value when they shop—even if they’re not economically concerned.

Younger shoppers are making room for splurges and trade-ups

Gen Z and Millennials are the most clever in their spending habits. While the proportion of shoppers managing costs is similar across generations, younger consumers are doing what they can to keep shopping.

49% of Gen Z and 39% of Millennials are making spend-expansive shopping changes. Only 23% of Gen X and 25% of Baby Boomers say the same.

Take action

For shoppers weighing their options, you have a chance to win them over:

- Use value tiebreakers in campaigns (like reviews and ratings, comparisons, loyalty perks, warranties, delivery speed, and easy returns) to give customers a reason to choose you when prices and products look similar.

- Promote bundles, subscriptions, free shipping, and gifts-with-purchase to cater towards value-seekers without relying on heavy discounting.

- Lean into VIP messaging and rewards programs to highlight other ways your customers can get more value from sticking with your brand.

Shoppers are prioritizing personal growth, experiences, and self-care & wellness

New Year’s resolutions are showing up in shoppers’ budget allocations. Personal growth, experiences, and self-care and wellness categories are seeing the biggest spending increases.

Note: This data is calculated based on shoppers who usually purchase in these categories.

Overall, consumers are spending the same or more in these categories over the next three months:

- 75%: Everyday essentials

- 66%: Self-care and wellness

- 65%: Gifts for others

- 65%: Personal growth and learning

- 54%: Hobbies and interests

- 54%: Experiences

- 53%: Tools and tech that make life easier

Where shoppers are pulling back the most: luxury purchases (61%), home comfort and upgrades (58%), and self-gifts (52%).

These categories are broad, and not specific to any one industry. So you can focus on products that suit these categories naturally—or position products to match shoppers’ buying intentions.

Gen Z and Millennials stay broad; Gen X and Baby Boomers narrow the list

Priorities change slightly across generations. Lean into these nuances to customize your approach depending on your target audience:

Gen Z is spending the same or more in most categories, except for the 50% that are cutting back on luxury purchases. So you can reasonably reach them from any angle.

Beyond daily essentials, Gen Z’s top priorities are:

- Personal growth (74%)

- Gifts (70%)

- Self-care and wellness (69%)

Millennials match on to Gen Z, with 52% cutting back on luxury.

Like Gen Z, Millennials are most interested in these categories after essentials:

- Personal growth (71%)

- Gifts (70%)

- Self-care and wellness (66%)

Gen X is more selective. They’re cutting back on luxury purchases (73%), home comfort and upgrades (68%), self-gifts (58%), experiences (54%), and products to make life easier (50%).

After the essentials, Gen X is interested in pulling out their wallet for:

- Self-care and wellness (65%)

- Personal growth (64%)

- Gifts (60%)

- Hobbies and interests (54%)

Baby Boomers have the most focused shopping intentions. They’re cutting back the most on luxury purchases (82%), home comfort and upgrades (74%), tools and tech to make life easier (61%), hobbies and interests (58%), experiences (56%), self-gifts (56%), and personal growth (55%).

Beyond essentials, Baby Boomers are prioritizing:

- Self-care and wellness (65%)

- Gifts (60%)

Take action

Map your promotions to shoppers’ buying intentions. Focus on products that naturally match where shoppers are spending and position your promotions from that lens.

Consider segmenting by product affinity or interest. Then send campaigns that match the top purchase motivations.

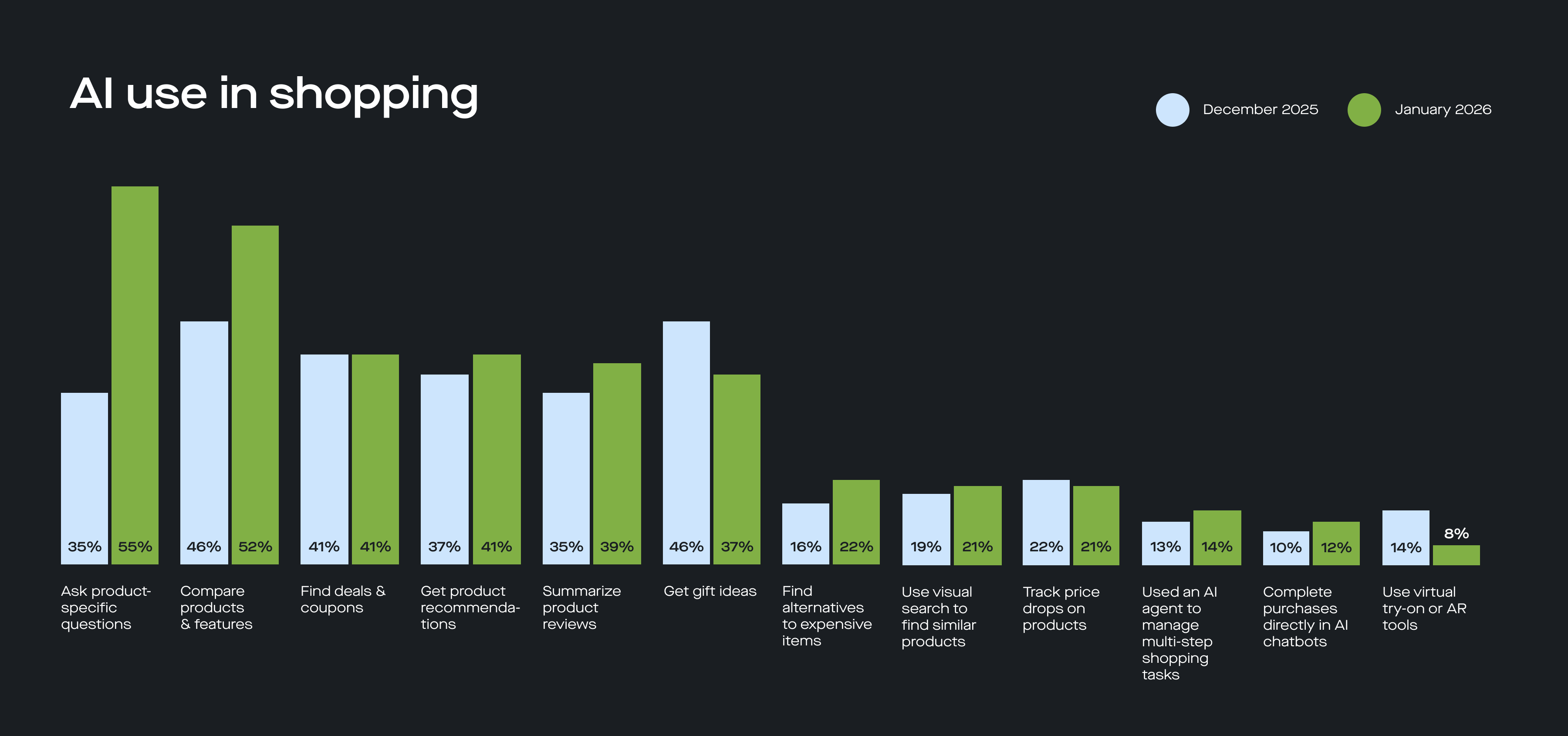

70% of consumers are using AI to help with shopping—from discovery to conversion

As shoppers weigh value and make more intentional purchase decisions, it’s rapidly becoming mainstream to use AI to shop smarter. 70% of all consumers say they used AI to help them shop in the last three months—close to the 72% of BFCM shoppers who said AI helped with their Cyber Week shopping.

This includes 90% of Gen Z and 82% of Millennials. Older generations are also getting on the bandwagon. 45% of Baby Boomers have used AI for shopping in the past three months—up from 34% who said they used it for Black Friday.

Of those who have used AI for shopping in the past three months, their top use cases are:

Smaller groups of shoppers are using AI in more advanced ways:

- 22% have used AI to find alternatives to expensive items

- 22% have tracked price drops.

- 21% have used visual search to find similar items

- 12% have completed purchases directly in AI chatbots.

Many AI use cases are up significantly from December.

Take action

AI use is expanding. Take advantage of this shift by updating your website (particularly your PDPs) with clear, structured content that makes it easy for LLMs to scan. Add clear specs, thorough descriptions, and comparison content to your website so AI tools are well-equipped to answer questions and surface your product when shoppers turn to chatbots for help.

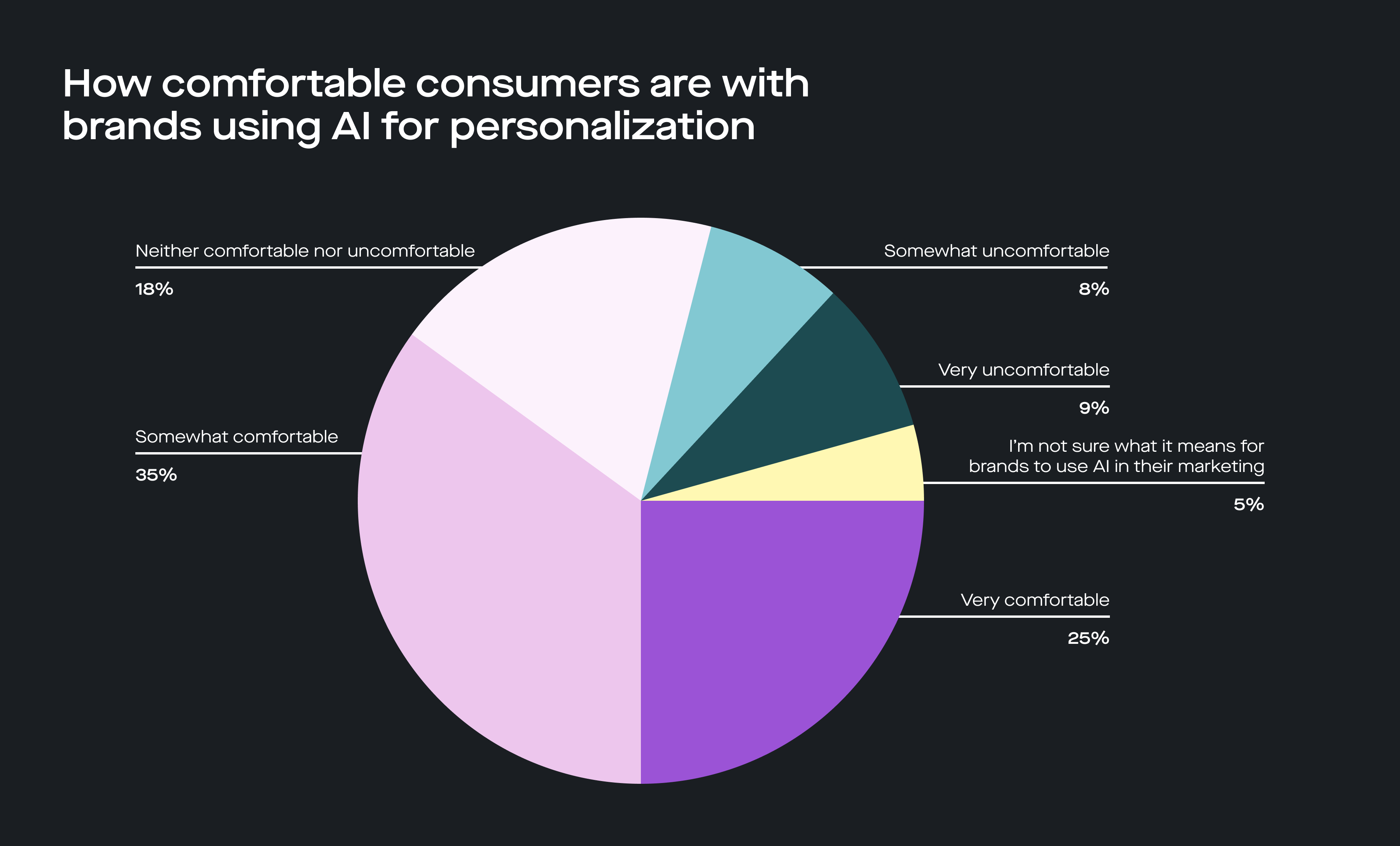

60% of shoppers feel comfortable with brands using AI for personalization

In an era of increased scrutiny around data collection and privacy, many brands are trying to balance the personalization consumers want with the caution they feel with sharing their data.

In The State of Personalized Marketing in 2025, we found that 64% of consumers are protecting their privacy. However, 71% want brands to learn from their shopping habits over time. They just want transparency and control around how their data is being used.

To take that a step further, though, how do shoppers feel about brands using AI for personalization?

This survey reveals that 60% of shoppers feel comfortable with brands using AI to personalize marketing messages and product recommendations. Only 17% feel uncomfortable with brands using AI. So overall, shoppers are embracing this new technology.

This is even more true for shoppers who use AI themselves. 77% of AI users feel comfortable with brands using AI to personalize their shopping experience (and only 7% do not).

Take action

AI helps marketers turn customer data into meaningful 1:1 personalized interactions that foster customer relationships and improve revenue and ROI.

To use AI in alignment with customer expectations around data privacy:

- Be clear about how you’ll use customer data and give shoppers control over their data and communication preferences.

- Collect and activate relevant first-party data that improves the customer experience so they see the value of allowing you to use their data.

- Use AI to scale message relevance beyond what humans can do alone with tools like Attentive’s AI Journeys for 200% more revenue on triggered messages AI Pro for 15% more SMS and email revenue, and AI Grow for 25% more subscribers.

The bottom line: Shoppers are weighing every purchase. Earn their attention by communicating value and staying AI-discoverable.

Even with 84% of shoppers concerned about the economy, many are maintaining their discretionary spend and finding ways to shop smarter.

The brands that will be best positioned to grow in 2026 will:

- Build confidence with clear value

- Map promotions to intent

- Prepare for AI-driven discovery

- Scale 1:1 personalization powered by AI

As value-driven and AI-assisted shopping become mainstays, you can use the rest of Q1 to lay the foundation for these initiatives and test what works, ultimately setting your brand up for success in 2026.

The Attentive Consumer Pulse: Attentive surveys 600 US consumers quarterly to help brands understand shifting consumer mindsets and behaviors and how brands can adapt their marketing strategies.