Consumers are more deliberate—but 87% of hesitant shoppers don’t need a discount to move forward. Here’s what to prioritize in Q2.

Economic concern has risen to 90%, up from 84% in January—and shoppers are comparing options more carefully, spending less on discretionary purchases, and being more deliberate before buying.

But these are challenges brands can overcome.

We surveyed 600 US consumers to find out what’s driving shopping behavior and how brands can overcome purchase hesitation.

The opportunities ahead:

- Multichannel subscribers are more likely to spend and stay loyal to brands—so it’s worth growing and investing in this audience.

- Triggered messages designed to overcome purchase hesitation—and backed by strong identity resolution—will help you act on shopper interest.

- Reinforcing quality and value in your campaigns will encourage shoppers to choose you.

- Aligning promotions to shopper priorities and real use cases can make your products feel like an obvious choice.

Read on to learn what’s driving shopping behavior right now—plus 6 action steps you can put to work in your email, SMS, and push program this quarter.

Economic outlook: 90% are concerned, but multichannel subscribers are ready to spend

Shoppers are feeling economic pressure, leading to more intentional spending.

90% of US shoppers say they’re concerned about the economy, up from 84% in January. Spending reflects that shift:

- 50% spent less on discretionary purchases in the past month, up from 42% in January

- 18% spent more, down from 28% in January

A closer look shows that shoppers are cutting back in some ways so they can spend freely in others.

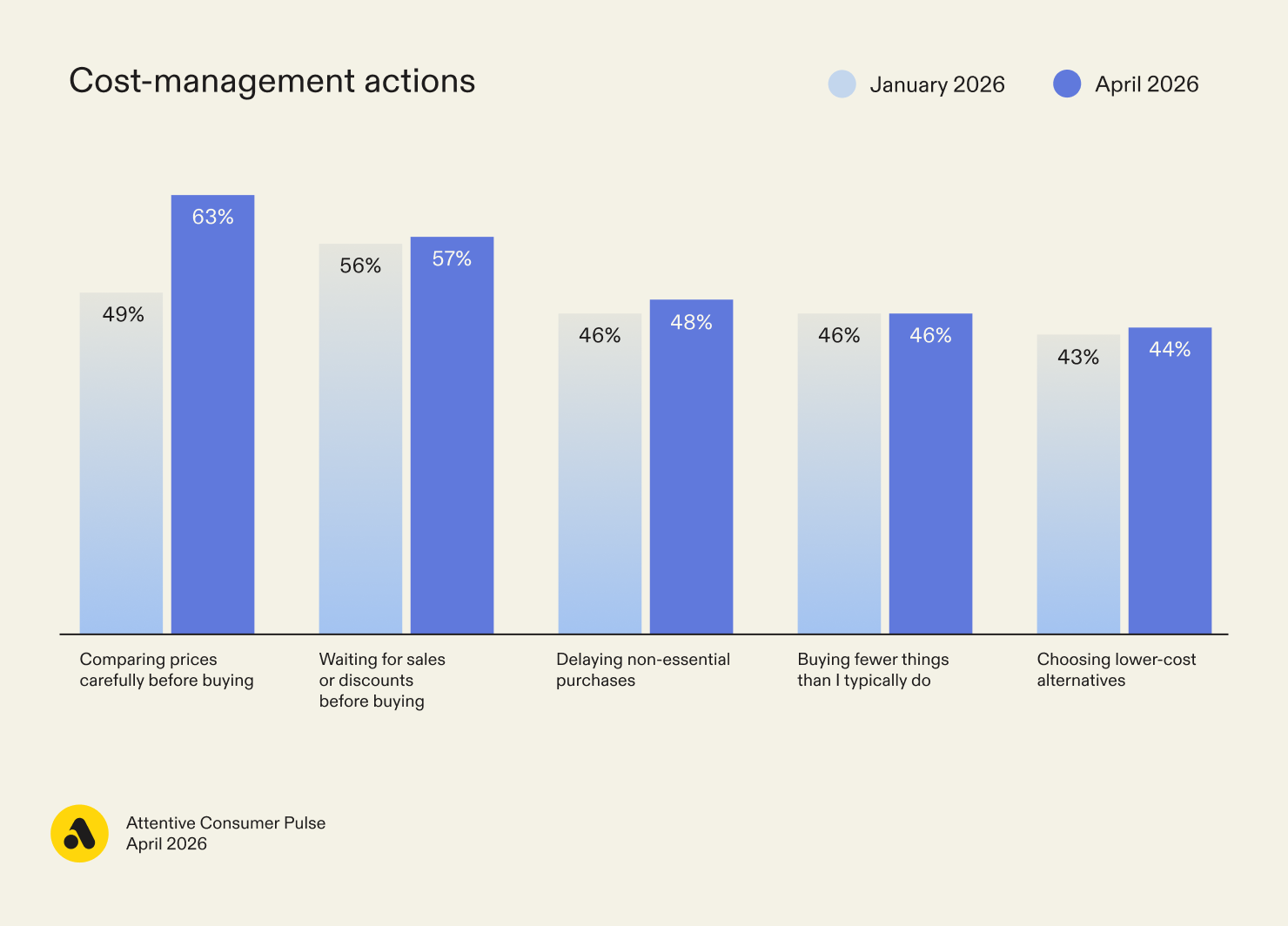

Managing costs: 63% are comparing prices carefully before buying

The clearest shift from January: more active price comparison. 63% of shoppers are comparing prices carefully before buying, compared to 49% in January.

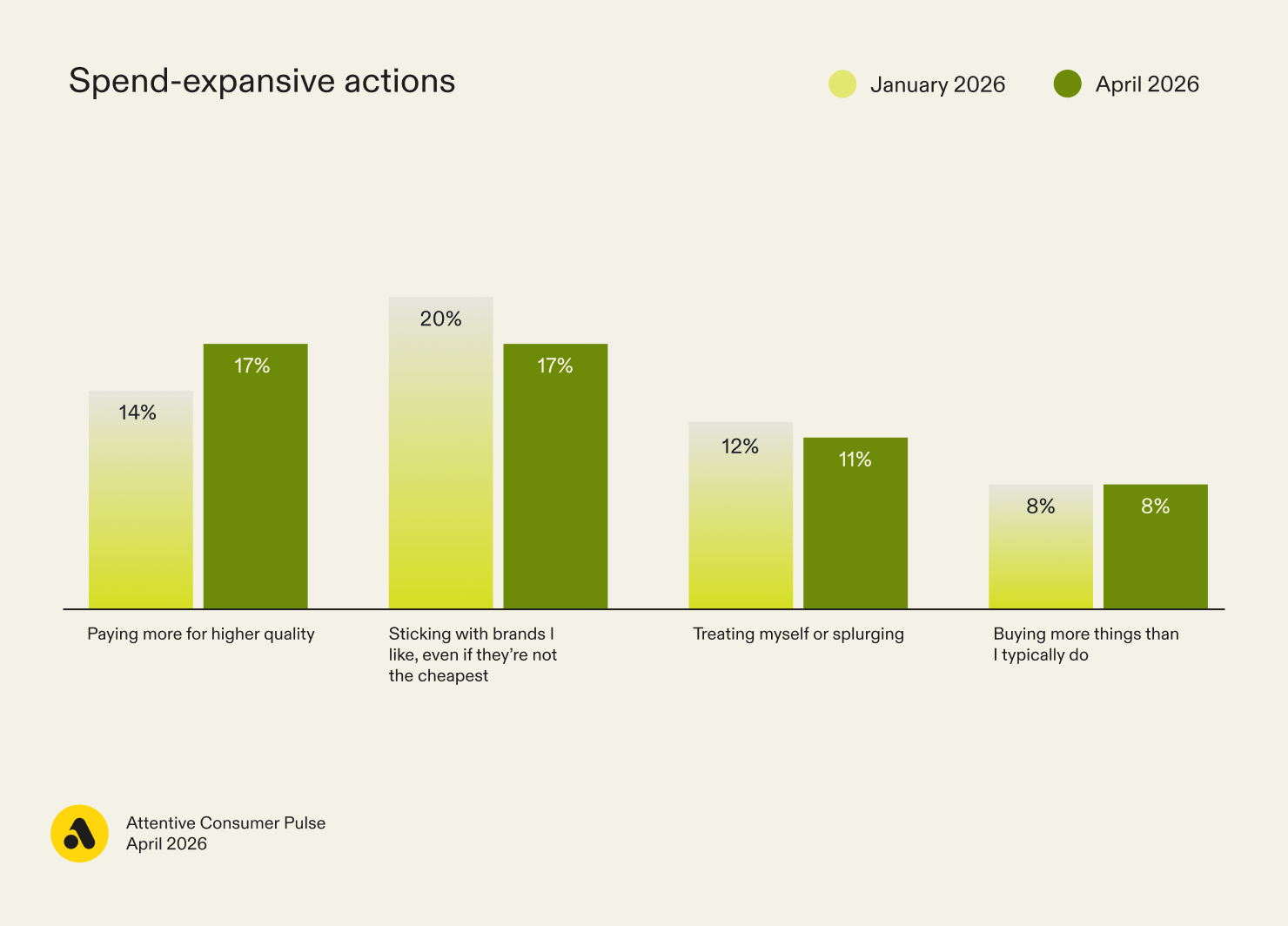

Spending more: Shoppers prioritize quality and brand preference

Spend-expansive behavior hasn’t changed much since January. When shoppers do spend more, paying for higher quality and sticking with brands they like remain the top reasons why.

Multichannel subscribers are more ready to spend

Subscribers on two channels—email, SMS, and/or push—are 1.8x as likely to take spend-expansive actions as single-channel subscribers. For those subscribed to all three, that rises to 2.8x.

This makes a strong case for growing your multichannel audience and giving those subscribers a more coordinated experience across SMS, email, and push.

Younger shoppers are making more deliberate trade-offs

Gen Z and Millennials are more likely than older shoppers to be managing costs—and taking spend-expansive actions.

This suggests that younger shoppers are being even more intentional—pulling back where they can to invest where they want to.

For brands, that creates room to position products as worth paying for in a value-conscious moment.

Overcoming purchase hesitation: 97% of hesitant shoppers can be moved to purchase—most don’t need a discount

97% of shoppers who are hesitating on a purchase can be encouraged to move forward—including 87% who can be influenced by something other than a discount.

That’s good news in an environment where brands are protecting margins.

When we asked shoppers what would make them move forward with a purchase they’re hesitating on, better prices or discounts top the list. But confidence boosters (reassurance about product quality or suitability) collectively influence 63% of shoppers:

All of these motivators can be added to abandonment flows to speak directly to shoppers who have shown interest but haven’t committed yet.

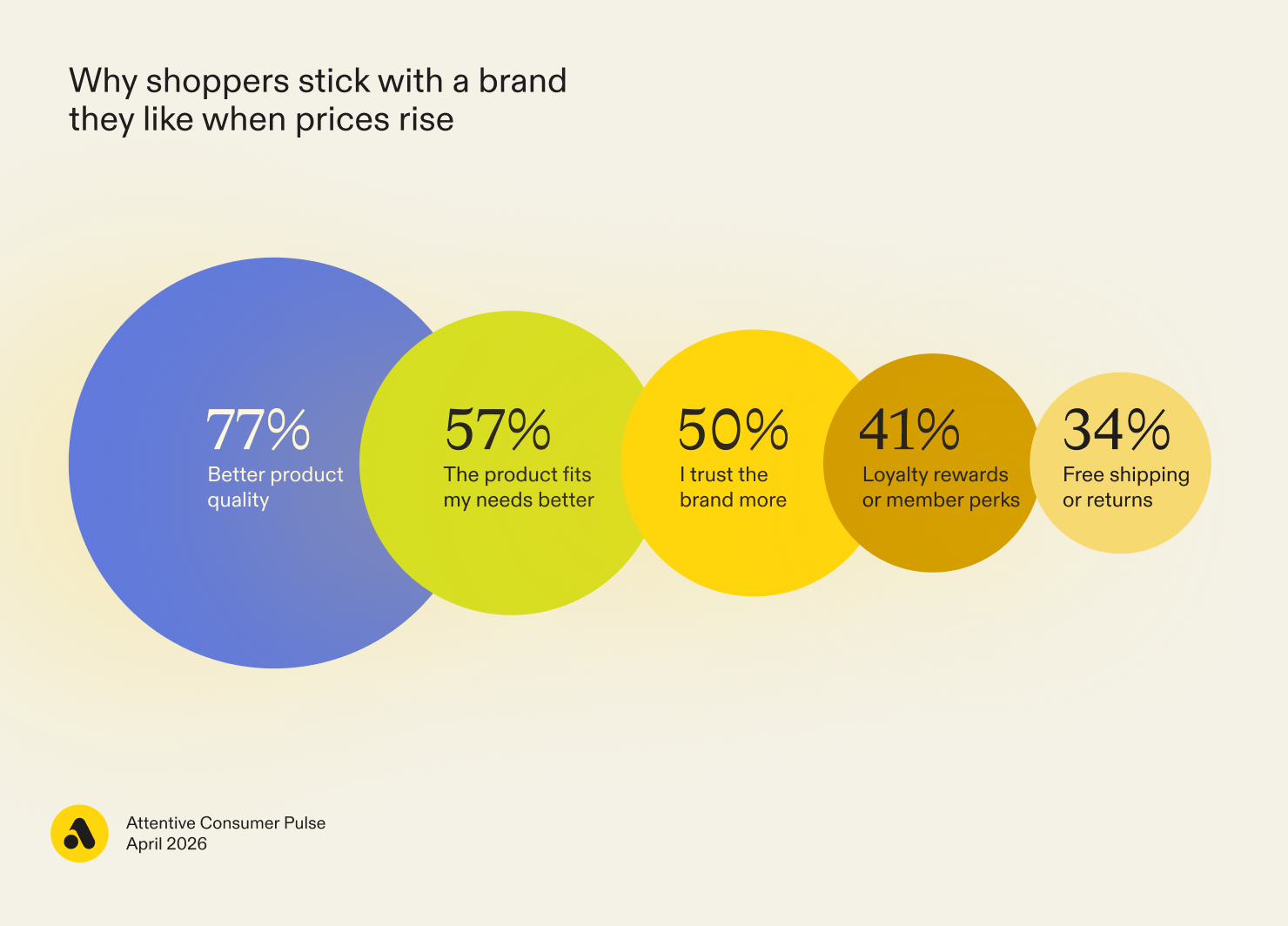

Loyalty is strong, but negotiable: 69% of shoppers stick with brands they like when prices rise

When prices go up enough for shoppers to notice, 69% of them (and 79% of Gen Z) try to stick with the brand in some form—only 8% switch to a cheaper alternative outright:

Notably, multichannel subscribers are meaningfully more likely to stick with a brand when prices rise—19% more likely for two-channel subscribers and 37% more likely for three-channel subscribers—rather than comparing alternatives or switching to a cheaper brand.

The top reasons shoppers stay with the brand they like when prices rise:

Each of these is a lever brands can pull in your messaging to earn and keep customer loyalty—especially when prices go up.

Learn what brings shoppers back: Read the 2026 State of Loyalty & Retention report.

Spending priorities: Practicality and ease are leading

Shoppers are spending their normal amount or prioritizing spend across most categories (among shoppers who normally purchase in each):

These categories are broad and not specific to any one industry. So you can promote SKUs that naturally fit, or position products to match these intentions.

Priorities are consistent across generations, with a couple of exceptions. Aside from practical everyday needs:

- Gen Z prioritizes home improvements over self-care in their top three.

- Baby Boomers prioritize gifts over personal growth.

Take action: 6 ways to win customers over in a cautious market

The data points to clear opportunities for brands to meet shoppers where they are. Here’s how to put it to work in your email, SMS, and push program.

1. Treat your multichannel subscribers as the VIPs they are

Shoppers subscribed across multiple channels are more likely to spend—and more likely to stick with a brand when prices rise.

A coordinated experience across channels converts that close relationship into revenue: 78% of brands with well-coordinated messaging programs report improved performance, compared to 50% of uncoordinated ones.

How to activate this:

- Send coordinated messages across channels. In an omnichannel program, channels inform each other—an SMS click improves the next email, a purchase suppresses a redundant push notification.

- Use each channel for what it does best. SMS and RCS for urgency and real-time moments, email for product education and storytelling, and push notifications for timely reminders that drive in-app action.

- Grow your multichannel list. In sign-up units, strengthen your welcome offer for shoppers that sign up for both email and SMS—and clarify the benefits of joining each channel. For existing one-channel subscribers, send dedicated campaigns encouraging them to add another channel.

Learn more: Omnichannel vs. multichannel: what's the difference?

2. Prioritize high-intent triggered messages to influence hesitant shoppers

Behavioral flows generally outperform individual campaigns—and as shoppers get more deliberate before purchasing, triggered messages can help you act on their interest in real time.

Most brands have the essentials (welcome, browse and cart abandonment, post-purchase), but fewer have additional triggers shoppers say move them to purchase: sale alerts, back-in-stock notifications, loyalty point reminders, and replenishment flows. Checkout and session abandonment are also worth adding to capture a broader range of the customer journey.

3. Invest in identity resolution to boost revenue

You can only send triggered messages to subscribers if you recognize them when they’re on your site. The more visitors you identify, the more high-intent moments you can act on, and the more revenue you can make.

In the 2026 Attentive Marketer Pulse, we found that 79% of brands actively investing in identity resolution report improved performance, compared to 59% of brands that don’t prioritize it.

Learn more: Why identity resolution is your biggest revenue opportunity

4. Audit your abandonment flows for impact

Hesitant shoppers are already signaling interest: visiting your site, browsing products, adding to cart. Your abandonment flows are the most direct way to address what’s holding them back:

- Discounts and pricing: If you’re offering a discount, highlight it throughout your flow. If you don’t want to lead with one, consider adding it later in the sequence for the most hesitant shoppers.

- Free shipping: If you offer it, say so. If you don’t, consider offering it selectively in flows as an incentive.

- Product confidence: Educate shoppers on your production process, materials, ingredients, or features—and tie these back to customers’ needs.

- Flexible payment options: Highlight Buy Now, Pay Later options if you offer them—particularly in checkout abandonment flows.

- Easy returns: Position your returns policy as a low-risk way to try out your products.

5. Reinforce your value to turn new shoppers into loyal customers

What keeps shoppers loyal when prices rise is a blueprint for turning new customers into repeat buyers.

Put it to work:

- Lead with product quality and fit: Emphasize the value you provide over alternatives and educate subscribers on what makes your product worth it. Tie features to how your product solves a real problem—and segment to speak to different customer motivations.

- Build trust: Customer testimonials, reviews, UGC, industry accolades, and third-party features all help establish early trust.

- Invite customers to your loyalty program: 41% of shoppers stick with a brand when prices increase because of the perks they receive—plus, the 2026 State of Loyalty & Retention report shows that seeing progress toward rewards is motivating for 81% of shoppers.

6. Shift your messaging to match how shoppers are spending right now

Practicality, time-saving, self-improvement, and self-care are all strong—big splurges and hobbies less so. Focus on products that naturally fit these categories and reframe how you position others in your campaigns.

For example, a mattress can be positioned as a practical long-term investment, a self-care essential for better sleep, or a tool for peak performance.

Next read: 68% of brands improved messaging performance YoY. Learn what separates them from the brands that didn’t.

Methodology

This survey was conducted online via Pollfish among 600 US adults from April 10–15, 2026. The study was designed to analyze results evenly across four generations: Baby Boomers, Gen X, Millennials, and Gen Z. Because younger respondents were harder to recruit in field, final results were weighted only by generation so that each one contributed equally to the overall analysis. No other post-stratification adjustments were applied.